Start A 401k For My Business – You’ve heard the term 401(k) or Roth 401(k), and you know it’s a great way to save for retirement. But how do you open a 401(k)? Are you able to start it yourself or does your employer have to start it for you? There are many questions related to pension savings. In this blog, we’ll answer five frequently asked questions about how to open a 401(k).

Let’s start with this important question. What is the purpose of a 401(k) and why should we open one? 401(k) plans are a great way to save for retirement because of the tax advantages. They have higher contribution limits than an Individual Retirement Account (IRA), and do not have income limits like an IRA. Often, 401(k) plans offer a Roth option, which allows you to grow your retirement savings tax-free, regardless of your income.

Contents

Start A 401k For My Business

401(k) accounts have many advantages. If you have access to one or can open it, this is a great tool to use! Read here for 8 401(k) benefits you may not know about and to learn more about the many benefits 401(k) plans offer.

Connect Guideline With Quickbooks Online

If you work for an employer that doesn’t offer a 401(k), you have other options for saving for retirement. A great place to start is maxing out your traditional IRA or Roth IRA each year. The 2023 maximum is $6,500 a year, well below what most people need to set aside for a secure retirement. That doesn’t mean you have to stop saving. You can add money to a taxable brokerage account with the intention of saving those funds for retirement. This account won’t have the same tax-deferred (traditional) or tax-free (Roth) options as a retirement account, but it can be a solid way to save and invest for your future.

If your employer is open to discussing offering a 401(k) to its employees, bring it up. They probably don’t know how easy it can be. Many employers don’t know that a business can get tax breaks by offering a 401(k) to employees. When a company offers employee benefits, it can also be a great retention tool for great employees. There are many reasons why a company might consider starting a plan, and an employer may just need some information and encouragement to get started. Tweet

If you are self-employed or own a business with no employees other than your spouse, you can open a solo 401(k). A solo 401(k) is sometimes called an automated 401(k). If you’re a sole proprietor, freelancer, or consultant, you may be able to set up a SEP IRA yourself. However, if you don’t meet any of these criteria, you can only access a 401(k) through an employer-sponsored plan.

A 401(k) is offered by your employer, so you usually can’t open a 401(k) on your own. If you’re self-employed, you may be able to open a 401(k) plan for yourself, called a solo or single-participant 401(k) plan. You can open a solo 401(k) on your own. solo 401(k) providers. If your business is just you or your spouse, these plans can be a great way to save for retirement, and they’re easy to set up! You can contribute as both an employee and an employer, so your contribution limits are higher than if you work for someone else. Learn more about Solo 401(k) plans here. Read on.

How To Set Up Your 401(k)

While you can’t open a 401(k) without an employer, you can take advantage of other tax-advantaged retirement plans without an employer. This includes opening a solo 401(k), traditional IRA, or Roth IRA.

It is best to discuss these options with a certified financial advisor to find the best one for you and your employment situation.

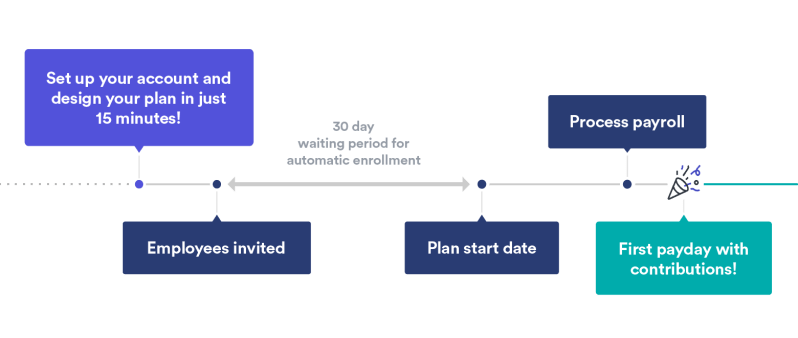

Small businesses have previously shied away from offering 401(k) plans for financial reasons. For years, 401(k)s were expensive for companies with many employees and therefore cost prohibitive for small businesses. But now there are many affordable options for small businesses. By offering a 401(k) plan as part of an employee compensation plan, small businesses can attract talented employees. There are some fees associated with setting up a 401(k) for your company, so it’s best to talk to 401(k) providers about the plan that’s best for your company.

When you start a 401(k) plan for your company, there may be a one-time setup fee. This fee will cover things like setting up the plan and educating company employees about the 401(k) plan. Additionally, there will likely be a monthly fee based on the number of participants and the amount of funds in the plan. The cost of the fee will depend on which 401(k) provider you choose.

Starting A Business With Your 401(k)? Be Careful.

To open a 401(k), you need to find a 401(k) provider to work with. There are many options, so you’ll want to know what your needs are before making a decision. Here are a few things to keep in mind when looking for a plan provider:

Transparent fees: How much will it cost you to use the service they provide? What does that involve? All of this should be transparent and clear when you talk to your plan provider. If they seem to sidestep the discussion of fees, it may be time to cross them off your list of potential suppliers. Also compare their fees and services with other providers, lower fees do not always mean they are a better option.

Services Offered: As an employer offering a 401(k) plan, you become responsible for the plan. This means that you maintain fiduciary standards, making decisions in the best interest of plan participants (your employees) at all times. This can be difficult for some employers unfamiliar with managing 401(k) plans. Know your limits, then find a plan provider that can help.

Many providers will offer full service and share fiduciary responsibility with you, but this comes at a cost. Interview service providers and find out what services you need. Then choose the one that suits your needs and budget.

What Is A 401(k) Plan?

Investment options: Make sure the 401(k) provider has a good selection of low-cost investment options for you and your employees. These will be the options plan participants can choose to build their retirement assets. A good selection at a low price should not be overlooked.

Companies aren’t required to offer a 401(k), but it can be a cost-effective way to compete for talented people in the workforce. About 51% of employers that offer a 401(k) also offer a matching contribution. Companies typically choose a 50% matching 401(k) contribution of up to 6% of employee salary. If you use a safe harbor 401(k), you must choose a specific employer matching scheme.

A safe harbor 401(k) is a type of 401(k) that avoids complex annual nondisclosure testing requirements. Without the 401(k) safe harbor, the employer is required to conduct a test each year to determine whether highly compensated employees or owners are disproportionately benefiting from the 401(k) plan. If so, the company is obliged to return the “excess” contribution to the employee. A safe harbor 401(k) is exempt from these tests.

Do I have to offer a 401(k) to all employees? You can exclude certain groups of employees from participating in the 401(k) plan. For example, some 401(k) plans require one year of service before an employee can participate in the plan. Others exclude part-time employees (those who work less than 1,000 hours per year) and youth workers (under 21). The exclusion must be reasonable and must not violate the minimum age and service requirements under section 410(a) of the Internal Revenue Code (IRC Sec.). If you offer a 401(k) plan to attract talented employees, it may be beneficial to offer it to all of your employees. Get advice from a financial planner about your 401(k) today!

The Solo 401k Benefits

Now that you know how easy it can be to open a 401(k) plan, put the plan into action! If you’re wondering how to take full advantage of your 401(k) or other retirement plans, or have other financial questions you need answered, schedule a free consultation with one of our financial advisors today. Schedule a consultation.

Kayla Welte, AFC®, ChFC®, CFP®, has been helping clients maximize their finances since 2009. With a background in financial education and counseling, Kayla is passionate about helping people prioritize and achieve their financial goals. Kayla is a financial planner at District Capital Management, a financial planning firm designed to help professionals in their 30s and 40s get their finances moving. Schedule a free discovery call.

District Capital is an independent, fee-only financial planning firm. We help professionals and entrepreneurs in their 30s and 40s raise their finances and maximize their money. We are based in Washington, DC and work with people almost all over the country. Whether you’re recently self-employed or have owned a business for years, you might be

Using my 401k to start a business, roll over 401k to start business, how can i use my 401k to start a business, 401k for my small business, 401k to start business, how to start a 401k for small business, start a 401k for my business, how to use 401k to start a business, how to start a 401k for my small business, how to start 401k for small business, start my own 401k, how to start my own 401k